All Categories

Featured

Table of Contents

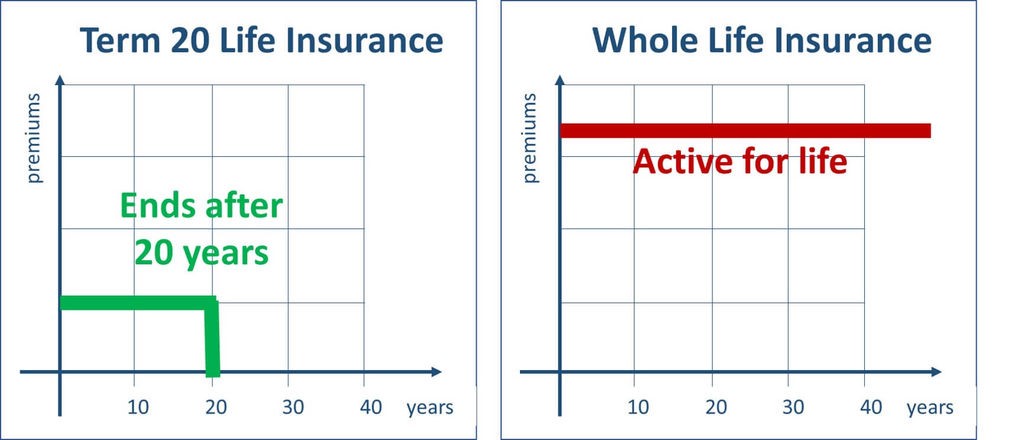

The are whole life insurance coverage and universal life insurance. The money worth is not included to the death advantage.

After ten years, the money value has actually expanded to roughly $150,000. He takes out a tax-free financing of $50,000 to begin a business with his bro. The policy loan rate of interest is 6%. He repays the loan over the next 5 years. Going this route, the passion he pays goes back into his plan's cash value instead of a banks.

Envision never having to stress regarding bank lendings or high passion prices again. That's the power of unlimited financial life insurance coverage.

There's no collection loan term, and you have the liberty to pick the payment timetable, which can be as leisurely as paying back the car loan at the time of death. This flexibility includes the maintenance of the car loans, where you can choose interest-only payments, keeping the funding equilibrium flat and manageable.

Holding money in an IUL dealt with account being credited rate of interest can often be far better than holding the cash money on down payment at a bank.: You've constantly imagined opening your own pastry shop. You can borrow from your IUL plan to cover the initial expenses of renting out a room, acquiring tools, and hiring personnel.

Infinite Banking Toolkit

Individual loans can be acquired from typical banks and cooperative credit union. Right here are some bottom lines to consider. Charge card can supply an adaptable means to borrow cash for very temporary durations. However, obtaining money on a charge card is usually very costly with interest rate of passion (APR) often getting to 20% to 30% or even more a year.

The tax therapy of policy finances can differ substantially relying on your country of house and the details terms of your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy car loans are normally tax-free, offering a significant benefit. Nevertheless, in other territories, there might be tax obligation implications to consider, such as potential taxes on the car loan.

Term life insurance coverage just gives a death benefit, with no cash worth build-up. This suggests there's no cash money value to obtain against. This article is authored by Carlton Crabbe, President of Capital forever, a professional in offering indexed universal life insurance accounts. The details offered in this post is for educational and educational functions just and need to not be taken as financial or financial investment suggestions.

Infinite Banking System Review

When you initially listen to about the Infinite Banking Idea (IBC), your initial reaction could be: This seems also good to be real. The issue with the Infinite Banking Idea is not the idea however those individuals offering an adverse critique of Infinite Banking as a concept.

As IBC Authorized Practitioners through the Nelson Nash Institute, we believed we would answer some of the top inquiries people search for online when learning and understanding everything to do with the Infinite Banking Idea. What is Infinite Banking? Infinite Financial was created by Nelson Nash in 2000 and totally described with the magazine of his book Becoming Your Own Banker: Unlock the Infinite Financial Idea.

How Does Infinite Banking Work

You believe you are coming out economically ahead because you pay no interest, yet you are not. With conserving and paying cash, you may not pay passion, but you are utilizing your cash when; when you spend it, it's gone for life, and you give up on the possibility to make lifetime substance rate of interest on that money.

Billionaires such as Walt Disney, the Rockefeller household and Jim Pattison have leveraged the homes of entire life insurance that dates back 174 years. Even banks utilize entire life insurance for the exact same purposes. It is called Bank-Owned-Life-Insurance (BOLI). The Canada Profits Agency (CRA) also acknowledges the worth of getting involved whole life insurance policy as a distinct property course used to produce long-term equity safely and naturally and supply tax advantages outside the range of traditional financial investments.

Infinite Banking With Whole Life Insurance

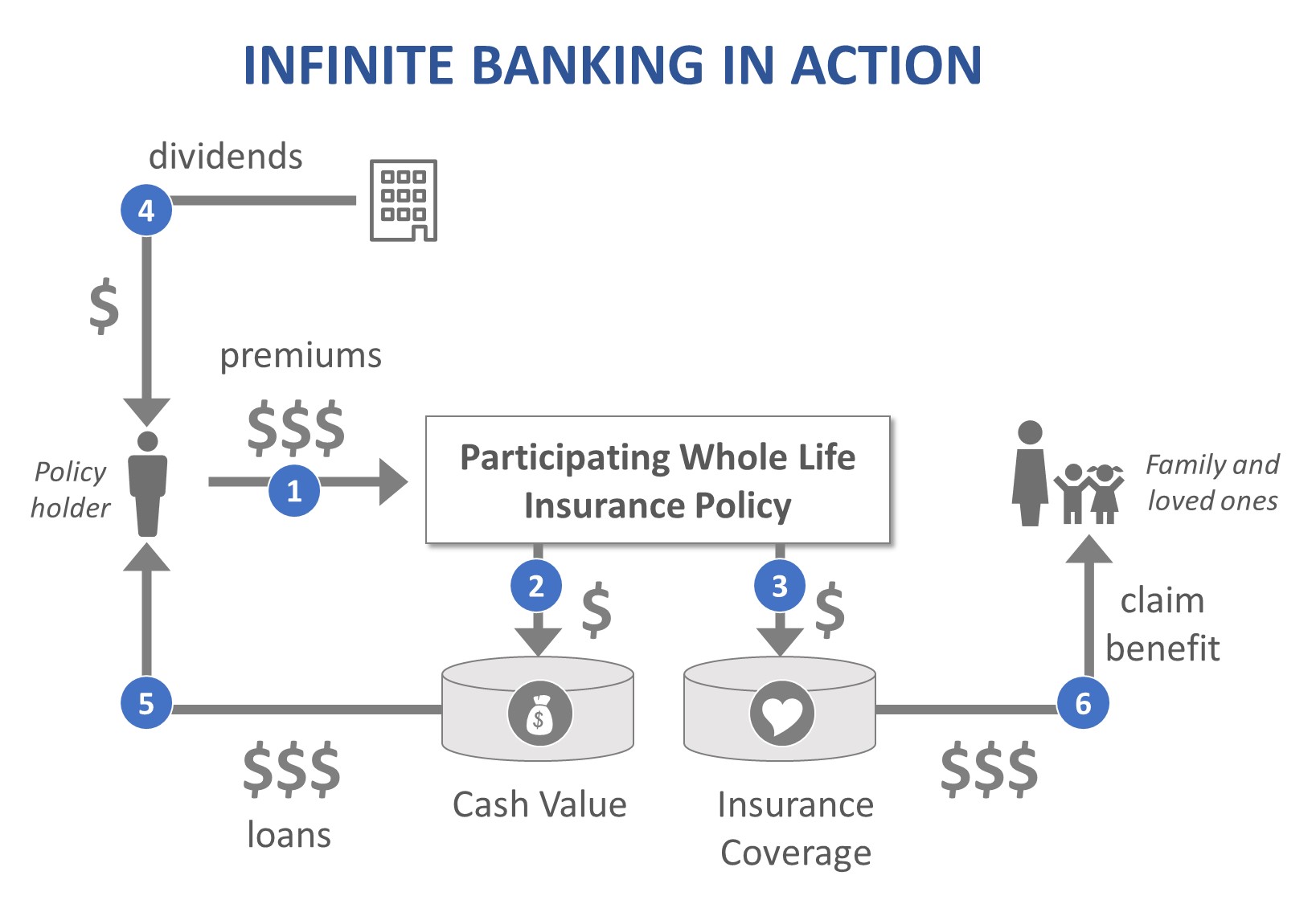

It permits you to produce riches by satisfying the financial function in your own life and the ability to self-finance significant way of life acquisitions and expenses without disrupting the substance interest. Among the most convenient ways to consider an IBC-type participating whole life insurance policy plan is it approaches paying a mortgage on a home.

Over time, this would produce a "consistent compounding" impact. You get the image! When you borrow from your taking part entire life insurance policy plan, the money value remains to expand uninterrupted as if you never obtained from it to begin with. This is because you are using the cash value and death benefit as security for a loan from the life insurance policy company or as security from a third-party loan provider (referred to as collateral financing).

That's why it's critical to deal with a Licensed Life Insurance policy Broker licensed in Infinite Banking who structures your taking part entire life insurance policy appropriately so you can avoid adverse tax implications. Infinite Financial as a monetary technique is not for every person. Right here are a few of the advantages and disadvantages of Infinite Banking you need to seriously think about in deciding whether to move forward.

Our recommended insurance policy carrier, Equitable Life of Canada, a shared life insurance policy firm, specializes in participating whole life insurance policy policies certain to Infinite Banking. Also, in a common life insurance coverage business, policyholders are thought about firm co-owners and get a share of the divisible surplus generated annually via dividends. We have a range of providers to select from, such as Canada Life, Manulife and Sun Lifedepending on the requirements of our customers.

Please also download our 5 Top Concerns to Ask An Infinite Banking Representative Prior To You Employ Them. To learn more regarding Infinite Financial see: Please note: The material provided in this e-newsletter is for informational and/or instructional purposes only. The info, point of views and/or sights revealed in this e-newsletter are those of the writers and not always those of the distributor.

Infinite Banking Examples

The concept of Infinite Financial was developed by Nelson Nash in the 1980s. Nash was a financing professional and fan of the Austrian college of business economics, which advocates that the value of goods aren't explicitly the result of standard economic structures like supply and need. Instead, people value money and goods differently based upon their financial condition and requirements.

Among the challenges of traditional banking, according to Nash, was high-interest rates on financings. Way too many individuals, himself consisted of, entered into financial trouble because of dependence on banking institutions. Long as banks established the rate of interest prices and loan terms, individuals didn't have control over their own riches. Becoming your own banker, Nash determined, would certainly put you in control over your economic future.

Infinite Financial needs you to own your monetary future. For ambitious individuals, it can be the most effective financial tool ever before. Right here are the benefits of Infinite Banking: Arguably the single most useful element of Infinite Financial is that it improves your cash circulation. You don't require to experience the hoops of a conventional bank to obtain a loan; merely request a plan financing from your life insurance policy company and funds will certainly be made readily available to you.

Dividend-paying entire life insurance is really low danger and supplies you, the insurance policy holder, a terrific offer of control. The control that Infinite Banking provides can best be organized into two categories: tax obligation benefits and property securities.

Entire life insurance policies are non-correlated assets. This is why they function so well as the economic foundation of Infinite Financial. Despite what happens in the market (supply, realty, or otherwise), your insurance plan keeps its well worth. Way too many people are missing this crucial volatility buffer that aids safeguard and expand wide range, instead dividing their cash into two buckets: checking account and investments.

Whole life insurance coverage is that 3rd pail. Not only is the price of return on your entire life insurance coverage policy assured, your death advantage and costs are also guaranteed.

Be My Own Bank

Infinite Banking allures to those looking for higher monetary control. Tax effectiveness: The money worth grows tax-deferred, and policy loans are tax-free, making it a tax-efficient tool for developing wealth.

Possession defense: In lots of states, the cash value of life insurance is shielded from lenders, including an extra layer of economic security. While Infinite Financial has its merits, it isn't a one-size-fits-all solution, and it includes considerable disadvantages. Below's why it may not be the very best technique: Infinite Financial usually needs detailed policy structuring, which can confuse policyholders.

{kind=link}

Latest Posts

Build Your Own Bank

How To Invest In Life Insurance Like Banks

Bring Your Own Bank: Expanding The Ways Companies ...